“We don’t recommend that one,” the broker told me. “It’s actually pretty low on our list.”

“Thanks,” I replied. “I appreciate that. But I’m going to go with it anyway.”

That was the final bit of an email conversation I had with a stockbroker at Ord Minnett Securities in New Zealand in late 1994. I’d just opened the first of what would ultimately end up numbering 12 or 13 brokerage and bank accounts overseas.

The broker was trying to warn me off a company called Fisher & Paykel, the maker of some of the dullest consumer goods on the planet: dishwashers, stoves, and similarly unsexy appliances.

Why anyone would send their money halfway around the world to own the likes of an appliance maker was beyond the broker’s capacity to imagine. Here we were… in the midst of a great tech boom… and this American yahoo (me) opens an account at the bottom of the world to own some company making stoves.

Moron.

Only… not really.

Supermodel vs. The Girl Next Door

I dove into Fisher & Paykel for two reasons:

- I suspected the appliance market in China and Southeast Asia—where F&P was a player—to boom as Asia’s middle class exploded (I was right).

- Making appliances is not a particularly tech-intensive business. Yes, there are improvements all the time, but at the end of the day, a wish/rinse/repeat cycle isn’t really going to change as dramatically as computer or telecom technology changes. Meaning that F&P was generating a lot of cash and sending it to shareholders as fat dividend payments because it didn’t have to spend extreme amounts on R&D.

By about 2008, when I wrote a book on global investing, Fisher & Paykel had sent me regular dividends, special dividends, and spin-offs that, combined, were worth well more than my original investment. The stock had soared and was just a few years off from being acquired at a premium price by China’s appliance giant, Haier.

The point here is that everyone’s idea of sexy is totally different.

Some of us want to chase flashy supermodels like Tesla and whatever AI stock is hot at the moment.

Some of us want the altogether cute but basic girl-next-door because we know reliability trumps flash-in-the-pan any day of the week.

In the world of Wall Street, the reliable girl-next-door is a solid company paying a solid dividend. It’s a stock like Fisher & Paykel at a time when the world was hung up on the early iteration of the internet.

Today is no different.

The Power of Dividend Investing

I’m looking at a list of top-performing stocks so far this year and it’s a bunch of IT companies like Diebold Nixdorf, IonQ, Applovin, Super Micro Computer, NVIDIA, C3.ai, etc. In fact, in the top 100 best-performing stocks of 2023 so far, I didn’t see a single company about which I can say, “Yep, that’s an entirely unsexy dividend payer.”

But here’s the thing: Dividends are far more important to the market than most investors realize.

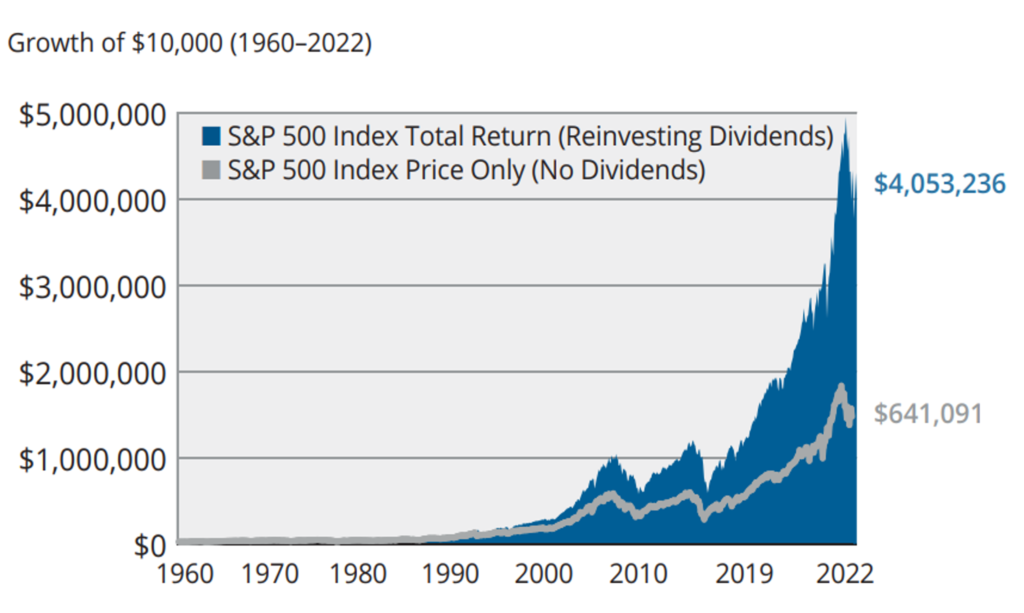

Mutual fund company Hartford Funds released a recent report titled, “The Power of Dividends: Past, Present, and Future.” And the big takeaway I want to share is this fact: Since 1960, 69% of Wall Street’s overall return has come from dividends.

Without dividends, a $10,000 investment in the S&P 500 back in the 1960s would have grown to $641,091 by the end of 2022. That’s a 7% annualized yield. Not shabby, but not spectacular.

Include dividends, however, and that same $10,000 in 1960 grows to $4.05 million by 2022… a 10.2% annualized yield.

Turns out the girl next door is actually the really sexy supermodel hiding behind sweats and a messy pony!

Dividend Investing Always Wins Over Time

Truth is, I’ve known for years and years that dividend investing is, arguably, the smartest take on investing. Hartford’s info is just updated data on a fact that has been floating around the Street for eons.

Indeed, I started investing for dividends in the earliest days of my nearly 40-year journey through Wall Street because I already knew the power of dividends back in the 1980s. It’s why I disregarded that Kiwi broker’s suggestion that I deep-six what was to him a dumb idea to own a maker of dishwashers and washing machines.

And it’s why I continue to disregard companies like Tesla and IonQ (some kind of quantum supercomputing gobbledygook… I had to look it up). They’re sexy in the same way that Pets.com and Webvan and other dot-com failures were sexy back in the mid- to late-`90s. Everyone wants to own them.

But as I told that stockbroker at Ord Minnet, “Thanks, but no.”

Going with the popular trends of the day is rarely a winning strategy unless you are a super-successful momentum trader… and 99% of the traders who say they are, aren’t.

I’d be willing to bet that by the end of this decade, a dull, crazy-boring, old-school company like Enterprise Products Partners, an oil-and-gas pipeline company paying a 7.4% annual dividend, will have performed better in a portfolio than will have Tesla.

It’s the power of dividends.

Unsexy as they are, they always win over time.